Last Updated on 2 years ago by Anoob P T

What to know about gift deed format? Here is everything you need to know when creating a gift deed including sample format, clauses, stamp duty and precautions when creating a gift deed.

Before proceeding with information about gift deed, if you are intertested in making money online, you can read some of our other posts.

Gift Deed: Format, Clauses, Stamp Duty & How to Draft Gift Deed

Table of Contents

What is a Gift Deed?

Simply speaking, Gift Deed is the official and legal document written for a gift.

When one person transfers a property, which can be either mobile or immobile, there needs a legal document stating this transfer of ownership in the form of a gift.

This law comes under Section 122 of the Transfer of Property Act, 1822 and protects the legal rights of both the donor and the recipient.

Even though it is legal, you should also note that this transfer of ownership needs to be completely out of love and should not have any form of cash transactions.

Gift Deed cannot be validated in the cases where there is even a slightest amount of cash transactions between the donor and recipient.

In Section 17 of the Registration Act 1908, it is mandatory to register immovable properties transferred to another person in the form of gift under Gift Deed.

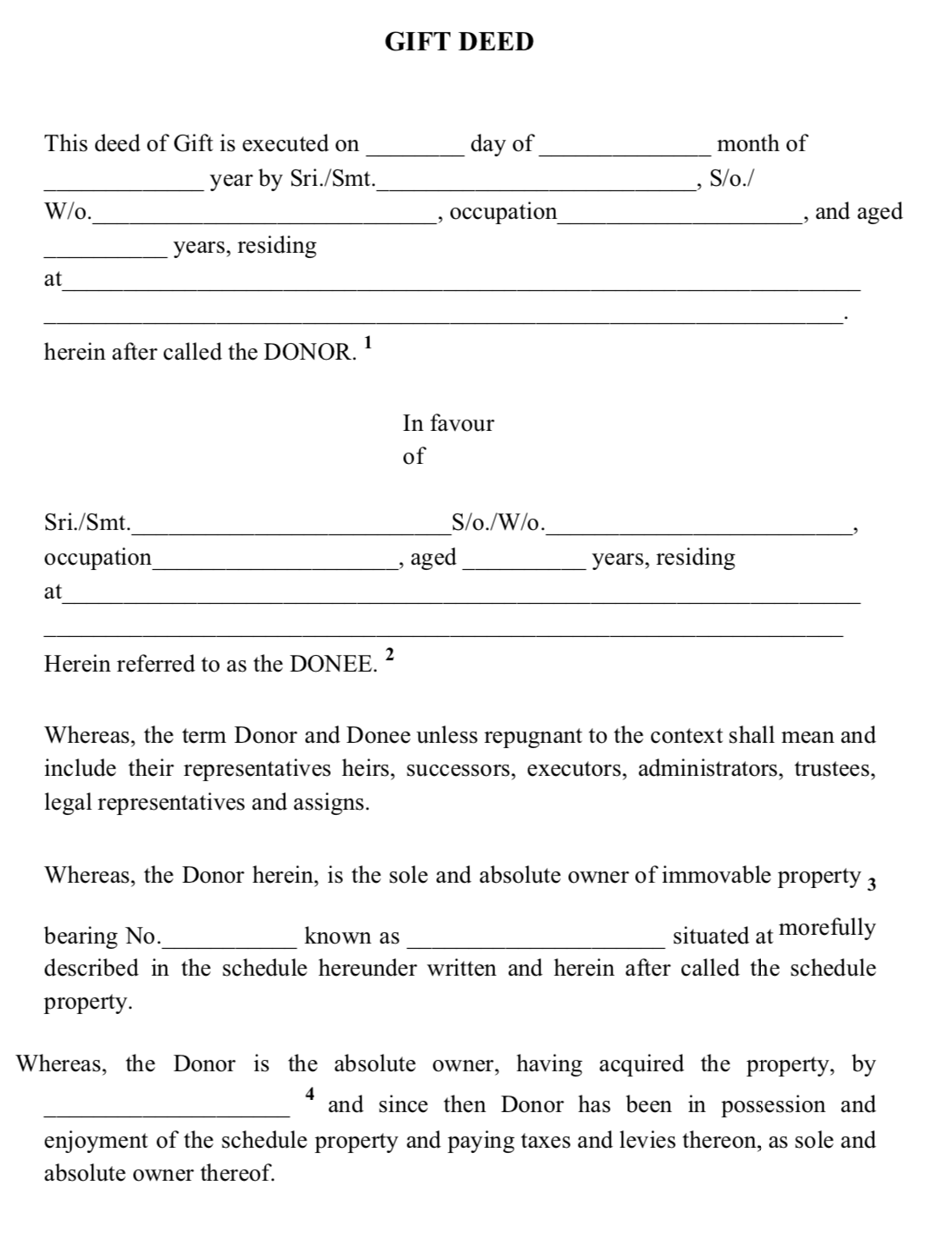

Sample Format of a Gift Deed

Important Clauses in a Gift Deed

- Free Will: it should be stated in the Gift Deed that the transfer of ownership is entirely as a gift and with the complete will of the donor. The donor should do it voluntarily and not under any threat or influence.

- Possession Clause: The property whether immovable or movable, can be transferred from the donor to donee only if it is under the ownership of the donor. The person who offers it as a gift should hold the title of owner for the property.

- Consideration Clause: There should not be any ash transaction involved between the donor and the done for the transfer of a gift. If there occurs any consideration in the form of money or alike, the property can no longer be considered a gift. The transfer should be out of love, without any sort of considerations involved.

- About Donor and Donee: The Gift Deed should clearly state the details of both the donor and donee as well as the relationship between them; if they are blood relatives or not.

- Information about the Property: The property which stands as the gift should be described in detail on the Gift Deed. The colour, location, area and similar details must be included.

- Rights and Liabilities: This legal document also includes the details about rights and liabilities concerning the property. It could mean the future uses or transactions related to the property like a sale or leasing it.

- Rights of the Donee: The rights of the donee has to be mentioned in relation with the property. These include his/her freedom to make any changes or innovations in the given property, rent the property or even considering it for sale. This clause allows the donee to enjoy the property peacefully without any further complications or liabilities.

- Delivery: The act of delivery or transfer of ownership hast to be clearly mentioned which confirms the possession of the property by its new owner.

- Revocation Clause: This clause avoids any future complications and it is advised to include it, even though not mandatory. Both the donor and donee has to agree on this clause.

Who are Donors and Donees?

A donor is a person who gifts the property to another person; be it his/her relative or a third party. You can transfer an immovable or movable property.

A donor should be of sound mind and has an age of above 18 years.

A donee is the person who accepts the gift from the donor.

He/she can be a relative or a friend of the donor. A person under 18 years can be a donee; however, the transfer of ownership goes to his/her parents till the person attains 18 years of age.

Steps Involved in the Drafting of Gift Deed

- A deed of gift can be drafted with the following information like

- Date and Place where the deed is to be executed.

- Information about Donor and Donee like Name, Residential Address, Relationship among them, Date of Birth, etc.

- Details about the property

- Two Witnesses

- Signatures of Donor and Donee along with the witnesses

- All the essential information has to be printed on a stamp paper and the stamp duty need to be paid depending on the respective state government.

- The final step is registration of the deed in the presence of a sub-registrar at the registration office.

Documents Required for Gift Deed Registration

Before registration, you have to sign the Gift Deed, attest it by witnesses and pay the stamp duty and registration charges.

The documents which must be shown for registration are:

- Original Gift Deed

- ID Proofs, like Driver License, Passport, etc

- PAN Card

- Aadhar Card

- A document like Sale deed to prove donor title to the Property

- Other Agreements which you might have entered into in relation to property

Other documents in relation with the property might also be required depending on your state policies.

Stamp Duty in Major States of India

The registration charges and stamp duty of each state in India varies according to the state policies. Some of those are given in the following box.

| State | Stamp Duty |

| Delhi | For Women 4% and Man 6% of the market value of the property. |

| Uttar Pradesh | 6% for Women and 7% for Man of the total value of the property |

| Karnataka | If the transfer is to non-family members it is 5.6% of the land value and in case of family members, it can range from 1000/- to 5000/- depending upon the property location. |

| Maharashtra | Family members – 3%Other Relatives – 5%If Agricultural land or residential property is gifted then it is Rs.200 |

| Gujarat | 4.9% of Market Value |

| West Bengal | 0.5% if transferred to family members and 6% in other cases.1% surcharge above 40lac. |

| Punjab | None in case of a blood relative or else 6% of property value. |

| Tamil Nadu | 1% for family members and 7% for other relatives |

| Rajasthan | Male -5%Female- 4% and 3% in case of SC/ST or BPLNone for Widow1% if it is in favour of wife or daughter2.5% in case close family members like son, daughter, in-laws, father, mother, grandson or granddaughter. |

What Type of Properties can be Gifted?

Any movable or immovable, existing, transferrable and tangible property can be given as a gift. in some states, you need not pay the stamp duty if you are gifting your property to an NGO.

However, some NGOs are exempted from receiving gifts and you will have to know about those.

You can transfer a property in order to help some one in crisis, as a favour, out of love or even to avoid any legal troubles associated with it.

For a donee, he/she should not that after the transfer of ownership, he/she is liable to pay any bills and alike associated with the property.

Can a gift deed be revoked or cancelled?

If there is no revocation clause, then a gift deed cannot be cancelled.

After the registration, the property becomes the sole right of donee and hence, the donor does not have a chance to cancel the ownership.

However, if a revocation clause which states that any specific incident or criteria if happens or is not followed, makes the Gift Deed invalid, then the agreement stands cancelled.

Similarly, the gift deed can be revoked if the donor claims of any act of threat resulting the transfer of ownership, which gets proved.

If the donor dies, his/her heirs have the right to file a revocation of the deed.

Income Tax Laws on Gift Deed

According to Income Tax Laws, any gift given by one person to another is exempted from income tax charges if the worth of total gifts do not exclude Rs.50,000.

If not, income tax will be deducted under “income from other sources”.

However, this rule does not apply if the persons are related by blood, i.e., parents, spouse, siblings, siblings of the spouse, lineal ascendants and descendants of the person and his/her spouse.

Some other people, organisation or condition exempted from this law are:

- in contemplation of death of the payer or donor, as the case may be; or

- from any local authority

- from any fund or foundation or university or other educational institution or hospital or other medical institution or any trust or institution referred to in clause (23C) of section 10; or

- from or by any trust or institution registered under section 12A or section 12AA; or

- by any fund or trust or institution or any university or other educational institution or any hospital or other medical institution referred to in sub-clause (iv) or sub-clause (v) or sub-clause (vi) or sub-clause (via) of clause (23C) of section 10; or

- by way of transaction not regarded as transfer under clause (i) or 20[clause (iv) or clause (v) or] clause (vi) or clause (via) or clause (viaa) or clause (vib) or clause (vic) or clause (vica) or clause (vicb) or clause (vid) or clause (vii) of section 47; or

- from an individual by a trust created or established solely for the benefit of the relative of the individual.

Frequently Asked Questions about Gift Deed Format

How do you write a gift deed?

Your gift deed format needs to have date, place, details about donor and the donee, details about property, ownership information and two witnesses.

Does gift deed require stamp duty?

No

How much does it cost for gift deed?

There are different rates for relatives and non-relatives, you need to check the charges for your state.

Who pays stamp duty in gift deed?

Donor is responsible for Stamp Duty

Recommended Reads